Student Loan Debt

Nearly one-third of all American students graduate with some student loan debt, with the average student graduating in 2020 with a debt of $38,792 resulting in a payment of about $400 per month. Collectively, these grads owe almost $1.6 trillion, according to the Federal Reserve Bank of New York. With Tuition Inflation growing and entry-level wages stagnant for graduates, the cost-benefit ratio for a degree is worsening while the benefits of a technical degree, Vocational school, or apprenticeship is growing. To make matters worse if you don’t actually finish the degree you have effectively paid for a piece of paper that you never got. Borrowers who don’t complete their degree have a harder time paying off their loans. Roughly 31% of people who took out student loans but didn’t complete either an associate or bachelor’s degree are currently behind on their payments.

The current student loan debt situation has taken on the proportions of a national emergency with experts wondering when the “house of cards” will come crashing down like the housing debt did in 2008. Although “late-stage delinquencies” (90+ days past due) have fallen drastically since 2008 i.e. from around 6% to about 1.5% in 2019 the topic has become a political football with Democrats like Sen. Elizabeth Warren (D-Mass.), Chuck Schumer (D-N.Y.) and Alexandria Ocasio-Cortez (D-N.Y.) —recommending canceling some or all student loan debt.

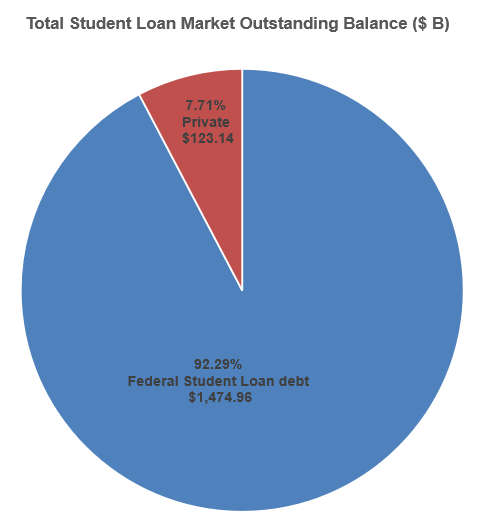

Over 92% of Student loans are backed by the Federal Government with only 7.7% from private lenders. Currently, it is difficult to get student loan forgiveness. It is one of the few classes of debt that can’t be eliminated through bankruptcy.

Pros and Cons of Debt Cancellation

Experts such as Moody’s Investor Service feel that eliminating student debt would stimulate the economy similar to a tax cut. Reducing the debt burden for these former students could boost real gross domestic product (GDP) by as much as $108 billion per year, according to one study from Bard College’s Levy Economics Institute.

However, other analysts warn that it is risky to create a precedent allowing people to transfer the cost of decisions to someone else. This could lead to even higher student debt burdens, as borrowers assume forgiveness will be ongoing. Other experts argue that forgiving student loans only provide a small stimulus to the economy because the savings are only realized in small amounts over a long period of time.

How Do You Get Student Loan Forgiveness?

The current forgiveness loopholes are only under very specific circumstances. If you are providing a service in a desirable situation such as a teacher in a low-income school or if you are in public service you may be eligible for forgiveness of a portion of your student loan debt. If you become disabled you may also be eligible for discharge of the debt. The federal government passed an emergency student loan relief measure that suspended repayments from March 2020, and the deadline has now been moved to Jan. 31, 2022. This however is a postponement of repayment, not a cancellation or even a reduction of the debt.

The following article originally appeared in 2012 but charts have been updated to include data current through October 2021. ~Tim McMahon, editor

Sky Rocketing College Costs

By Gordon H. Wadsworth

June 14, 2012

In the 19 years that I have been directly involved with college financial aid, I have heard hundreds of students and parents ask the same question, “How do I pay back those expensive student loans?” Just recently, a woman called asking for help. She told me she has loans dating back to the early 1980’s. All I could do was pray with her. There are no easy fixes. Having student loan debt is like owing money to the IRS. Once caught in the snare, there is no way out.

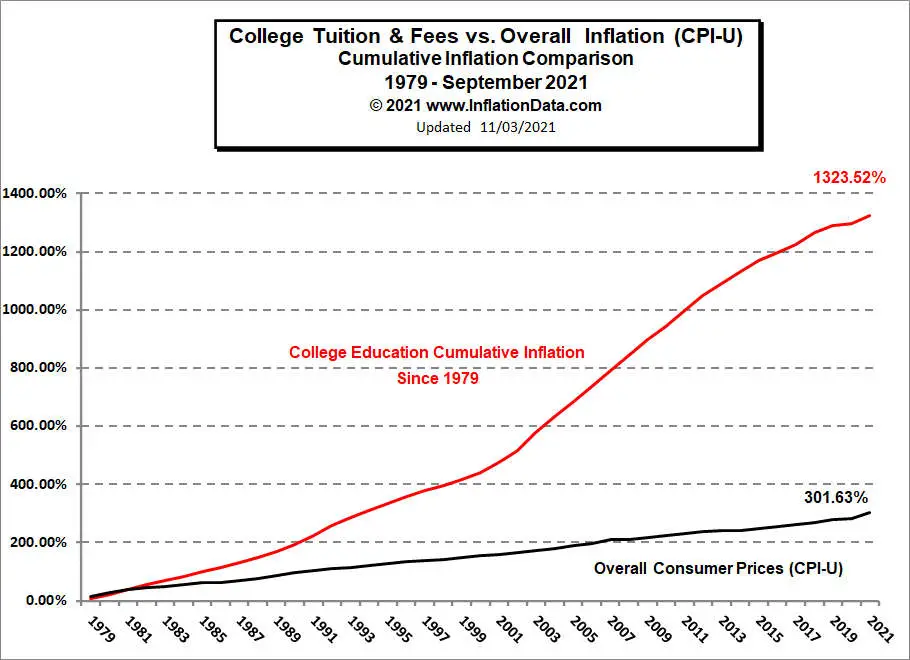

College tuitions soar each year, advancing far in excess of the inflation rate.

Editor’s Note: This chart shows cumulative CPI inflation vs. cumulative tuition inflation from 1979 through 2021. As you can see CPI-U inflation increased just over 300% from 1979 through 2021. This is bad enough. A 300% increase means that something that cost $1 in 1979, now costs $4.

But College Tuitions increased by a whopping 1000% MORE THAN THE CPI! In other words, for every $100 of tuition in 1979 it will now cost $1,423!

See chart below.

Many schools have increased tuition fees due to higher overhead costs. Fuel and labor costs continue to rise. Many older college buildings are in need of renovation or replacement. The demand for expanded libraries and new research and computer labs is at an all-time high. Some schools also need additional security measures.

Why Tuitions Increased Much More Than Inflation

Yet, the main reason tuition continues to rise is a dramatic change that took place regarding the Federal Stafford Loan more than a decade ago. When Uncle Sam opened the floodgates to government-backed student loans without parent income restrictions in 1992, colleges welcomed the news with open arms. The sudden injection of millions of additional aid dollars only furthered tuition increases. Add to that the government’s continued promotion of the Stafford Loan as a low-cost program, and you have the formula for hyperinflationary costs.

When the government made it exceptionally easy for students to borrow massive amounts of money, the colleges followed the lead by increasing their tuition rates.

Editor’s Note: Did you get that? When the Government tried to fix the Education system by throwing money at it, all that happened was Education got more expensive.

This combination led to record-level borrowing. Today [2012] the average undergraduate student loan debt is nearing $20,000.

- Average student loan debt in 2021 = $38,792

- Average student loan payment in 2021 ≅ $400/month

Those who go on to graduate school [2012] often end up with an additional $30,000. Law and medical students report an average accumulated debt from all years (undergraduate and graduate study) of $91,700. There are alternative options to amassing huge students loans such as attending an online university.

I introduced The College Trap, a new book packed with Internet links to scholarships, grants, and alternative ways to pay for college. People have already questioned the title. Some suggest that while many students are in financial bondage, it is not the fault of the higher education system.

True, there is more money available today for those wanting an advanced degree. The colleges talk in terms of big financial aid packages, but it is what makes up the aid package that is important. Often when students receive a multi-thousand dollar offer, it may be nothing more than a package of expensive student loans. The media refers to these as low-cost student loans, but they are not low-cost when you face debt of $20,000 or $30,000 at graduation.

For Tips from Gordon on how to save on education costs see his article Save on Education

For more articles on Education Inflation See:

- How Insidious Inflation Affects the Affordability of Tuition and Fees

- 8 Steps to Cut Education Costs

- Kids Going to College? Ease the Financial Burden

- Online Degree More Affordable Than on Campus

- Cutting the Cost of College

- Tips for Landing a Job with No Experience

- Paying for College: Student Loan Tips for the Newbie College Grad

- Mounting Debt and Lower Salaries – A Persisting Trend for Grads

- Great Jobs for Those with a College Degree

- Stay Ahead of Your Competition With Online Continuing Education Courses

- What to Look for in an Online Degree Program